The 5 Key Benefits of Debt Consolidation You Need to Know

Whether it’s to buy a new car or pay for your education, debt happens and can quickly lead to high interest rates and hard-to-manage monthly bills on your credit cards or loans. While this can sometimes be inevitable, it’s really how you choose to handle your debt that counts.

Debt consolidation is one strategy that exists that can make managing your debt far simpler by by rolling all of your debt into one single payment. It often comes with a lower interest rate than what you were paying out each month before while also giving your credit score a nice boost, among other benefits.

Some effective ways to consolidate your debt include taking out a personal loan, transferring multiple credit card debt into a single credit card, using a home equity loan, or even a 401 (k) loan.

Let’s take a closer look at what debt consolidation can do for you.

#1 Turn Multiple Payments into a Single Payment

Debt consolidation makes paying down your debt much more simple and can even result in lower monthly payments due to a longer pay off period. If you’re like most people with multiple credit card balances, consolidating everything into one single source will feel like a weight has been lifted off your shoulders. Sure, your debt still exists and hasn’t been reduced magically, but with multiple payment deadlines now gone, you can focus on just one debt source.

#2 Lower Interest Rates

Most unsecured debt—especially from credit cards—will have high-interest rates that can add significantly to the debt you have to pay each month. By paying off multiple high-interest debt accounts and rolling them one, you’ll be paying less in the long run by securing a lower interest rate on your new single account, if you have good to excellent credit.

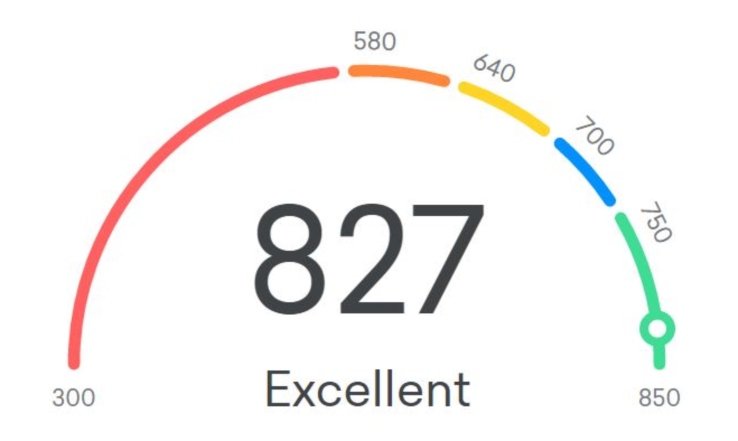

When it comes to finances, credit score is key and is a big determining factor in what kind of interest rate you can expect to secure when consolidating debt. The average interest rate for those carrying excellent credit (720-850) can range anywhere from 4-20% compared to those with poor credit (300-639) who might end up paying 15-36% on their consolidated debt.

Whichever credit score bracket you find yourself in, chances are the interest rate will still be lower than what you’re currently paying.

#3 Can Improve Your Credit Score

Speaking of credit scores, another benefit of debt consolidation is that it can give your score a nice boost. If you consolidate by taking out a personal loan, it’s likely that you will see an increase in your score in only a few months since you’ll be reducing your credit utilization rate (also known as credit utilization ratio).

This number comes from how much you owe right now divided by your credit limit. If you have a total of $5,000 in credit still available on two different credit cards, with a balance of $2,500 on one of them, your credit utilization rate is 50%, since you’re using half of the total available credit. Credit utilization plays a significant role in your overall credit score.

Keep in mind, however, that it’s normal to see a small, temporary dip in your credit score any time you acquire new credit, but the long-term gains you’ll see in both your credit score and savings on interest when consolidating debt make it a financially sound move.

#4 Less Stress

Consolidating your debt into a single, manageable payment will greatly reduce your stress and help clear up the clutter that multiple payments can very much feel like. Money matters like debt are known to lead to stress, but they don’t have to. By taking control of your finances and allowing yourself to stay on top of a single monthly debt payment, you’ll clear up your mind and find yourself in a better financial position.

#5 Pay it Off Faster

It’s not uncommon for credit card balances to have years to go before being fully paid off. After all, credit cards are earning interest on what you owe, so lenders don’t care if it takes you 5 years to pay off your debt or 20. A benefit of debt consolidation is that the consolidation process takes multiple factors into consideration when establishing the length of the loan, such as income, credit score, and how much you owe in order to come up with a sensible payback plan. For this very reason, debt consolidation loans have a shorter payback period.

Final Thoughts

Just like any other financial step, you’ll want to carefully evaluate your own situation to determine if its the best move for you, but there are significant gains to be had through debt consolidation that makes it a worthwhile option to consider.

It will bring together your debt sources into one simple monthly payment with a lower interest rate, it can help boost your credit score, and it will allow you to focus on other, more important things.

* Please consult with your attorney, financial consultant/planner, accountant, and/or tax advisor for advice concerning your particular circumstances. The information contained herein is for general informational and educational purposes only and should not be construed as professional, tax, financial or legal advice or a legal opinion on specific facts or circumstances. The information or opinions contained herein should not be construed by any consumer and/or prospective client as an offer to sell or the solicitation of an offer to buy any particular product or service.